We’re often asked the best way to sell a business. There are two key components at play in the sale of a business; structuring the transaction and positioning the business to the market. Both elements are important and can significantly impact your result.

Structuring the transaction covers things such as pricing the business, the terms and conditions attaching to the sale, key terms in the contract, and ensuring the transaction structure is as tax effective as possible. Much of the structuring is about ensuring the vendors secure the most efficient and effective outcome from the sale. It is about maximising vendor position.

Positioning is about doing everything needed to maximise the probability of a sale occurring, whereas structuring is about getting the best outcome from a transaction once it has occurred. A lot of people make the mistake of spending most of their energy on the structuring of the transaction. It is important but it only becomes important if the sale is achieved.

Positioning is about doing everything needed to maximise the probability of a sale occurring whereas structuring is about getting the best outcome from a transaction once it has occurred. A lot of people make the mistake of spending most of their energy on the structuring of the transaction. It is important but it only becomes important if the sale is achieved.

Discuss structuring first to help identify any key decisions that need to be made but put most of your effort into positioning the business.

To do this, you need to get an objective assessment of how the business compares in its market, its competitive position, and what, if any, impediments to sale exist – all the things a buyer will look at and look for when they assess your business. Most buyers believe that we are currently in a buyer’s market and will try to drive down price expectations. Whether or not you are in a buyer’s market depends on your industry segment but regardless of this, you are in a competitive market. Buyers may be comparing your business with similar businesses but also opportunities in other industry segments. Securing a sale at the best possible price is about having your business positioned for sale. Preparation time is needed to achieve this so talk to us well in advance of putting your business on the market.

Thinking of selling your business? Talk to us today about how to achieve the best possible outcome.

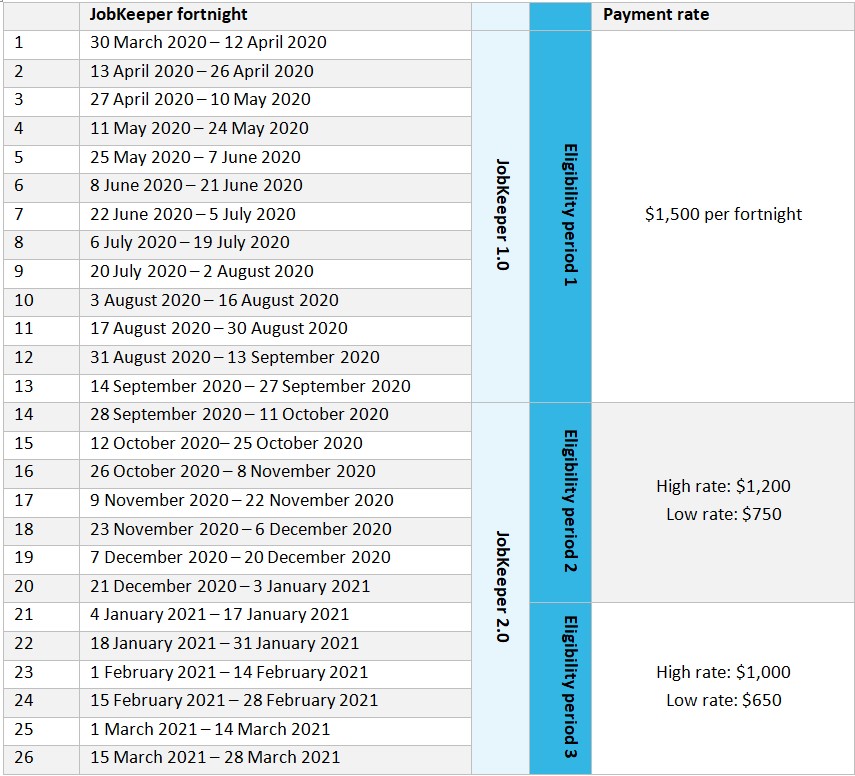

The first tranche of JobKeeper ends on 27 September 2020. Those needing further support willneed to reassess their eligibility and prove an actual decline in turnover.

To receive JobKeeper from 28 September 2020, eligible employers need to assess their decline in turnover with reference to actual GST turnover for the September 2020 quarter (for JobKeeper payments between 28 September to 3 January 2021), and again for the December 2020 quarter (for payments between 4 January 2021 to 28 March 2021).

From 28 September 2020, the JobKeeper payment rate will reduce and split into a higher and lower rate based on the number of hours the employee worked in a specific 28 day period prior to 1 March 2020 or 1 July 2020.

To access JobKeeper payments from 28 September 2020, there are three questions that need to be assessed:

Is my business eligible?

Am I and/or my employees eligible? and

What JobKeeper rate applies?

We’ve summarised the key details in this update.

Let us know if we can assist you in any way.

From 28 September 2020, the eligibility tests to access JobKeeper for employers will change, as will the amount of the JobKeeper payment for employees and business participants. To receive JobKeeper from 4 January 2021, employers will need to assess their eligibility again.

Eligibility for one JobKeeper period does not entitle you to, or exclude you from, payments in another period. Each eligibility period is addressed separately. That is, there might be businesses that qualified for the first tranche of JobKeeper, don’t qualify for the second tranche but qualify for the third.

On 1 March 2020, carried on a business in Australia or was a non‑profit body pursuing its objectives principally in Australia; and

before the end of the JobKeeper fortnight, it met the original decline in turnover test*:

15% or more

50% or more

30% or more

ACNC-registered charity (excluding universities, or schools within the meaning of the GST Act – these entities need to meet the basic turnover test)

Large businesses where aggregated turnover for the test period is: likely to be $1 billion or more; or aggregated turnover for the previous year to the test period was $1 billion or more A small business that forms part of a group that is a large business must have a >50% decline in turnover to satisfy the test.

All other qualifying entities

And, was not:

on 1 March 2020, subject to Major Bank Levy for any quarter ending before this date, a member of a consolidated group and another member of the group had been subject to the levy; or

a government body of a particular kind, or a wholly-owned entity of such a body; or

at any time in the fortnight, a provisional liquidator or liquidator has been appointed to the business or a trustee in bankruptcy had been appointed to the individual’s property.

1 March 2020 is an absolute date. An employer that had ceased trading before 1 March, commenced after 1 March 2020, or was not pursuing its objectives in Australia at that date, is not eligible.

one partner in a partnership, adult beneficiary of a trust, director or shareholder who works in the business (i.e., only one person in a partnership, one beneficiary of a trust, or one director / shareholder are eligible for JobKeeper payments).

will be eligible for the JobKeeper payment if the following conditions are met:

The entity carried on a business on 1 March 2020 and is not a not-for-profit entity; and

Had an ABN on 12 March 2020; and

Had some business income in the 2018-19 income year included in a tax return that was lodged by 12 March 2020; or made some supplies connected with Australia in a tax period that started on or after 1 July 2018 and ended before 12 March 2020 and notified the ATO of this (e.g. on an activity statement lodged with the ATO) by 12 March 2020. The Commissioner can potentially extend the deadline for holding an ABN, lodging the 2019 tax return or lodging a relevant activity statement.

Passed the decline in turnover test; and

The individual was not:

employed by the business at any time in the relevant fortnight; or

a permanent employee of another entity at the time the individual gives the nomination notice (i.e., they do not hold a full time or part time role with another employer); or

a nominated JobKeeper employee of any other business; or

entitled to parental leave pay or dad and partner pay or workers’ compensation payments for being totally incapacitated for work.

As at 1 March 2020, the individual satisfied all of the following:

Aged 16 years or over; and

If they are aged 16 or 17 years, they are either financially independent or are not undertaking full-time study;

Actively engaged in the business; and

An Australian resident under the Social Security Act or an Australian tax resident who holds a special category visa **

If the criteria have been met, the individual is eligible if they were actively engaged in the business in the fortnight of the JobKeeper payment, and they agreed to be nominated for JobKeeper payments and confirmed they pass the eligibility criteria.

If more than one director wants to access JobKeeper payments, they need to meet the eligibility criteria of an employee (see Eligible employees). To be an employee a director would have received salary/wages and this has been reported as salary/wages on activity statements, payment summaries, tax returns etc. If a director merely receives a distribution from the business then they are unlikely to be an employee.

For businesses already enrolled in JobKeeper, to receive payments from 28 September 2020, you need to meet an extended decline in turnover test based on actual GST turnover.

Businesses that are enrolling for the first time, need to meet the basic eligibility test and the decline in turnover test/s for the relevant period.

30 March to 27 September 2020

28 September to 3 January 2021

4 January 2021 to 28 March 2021

Decline in turnover test

Projected GST turnover for a relevant month or quarter is expected to fall by at least 30% (15% for ACNC-registered charities, 50% for large businesses) compared to the same period in 2019.*

Actual GST turnover in the September 2020 quarter (July, August & September) fell by at least 30% (15% for ACNC-registered charities, 50% for large businesses) compared to the same period in 2019.*

Actual GST turnover in the December 2020 quarter (October, November & December)fell by at least 30% (15% for ACNC-registered charities, 50% for large businesses) compared to the same period in 2019.*

* Alternative tests may apply

Most businesses will generally use their Business Activity Statement (BAS) reporting to assess eligibility. However, as the BAS deadlines are generally not until the month after the end of the quarter, eligibility for JobKeeper will need to be assessed in advance of the BAS reporting deadlines to meet the wage condition for eligible employees.

The ATO has the power to extend the time an entity has to pay employees in order to meet the wage condition. For the JobKeeper fortnights starting 28 September 2020 and 12 October 2020 the ATO is allowing employers until 31 October 2020 to meet the wage condition for all employees included in the JobKeeper scheme.

Calculating GST turnover for tranches 2 and 3 of JobKeeper is different to the original JobKeeper requirements as entities will only be using current GST turnover figures (not projected GST turnover).

When applying the new turnover reduction tests for the September 2020 quarter and December 2020 quarter, entities that are registered for GST must use the same method that is used for GST reporting purposes. That is, if the entity is registered for GST on a cash basis then a cash basis needs to be used to calculate current GST turnover for the purpose of these new tests. Entities that are not registered for GST can choose whether to calculate GST turnover using a cash or accruals basis, but must use a consistent method.

Current GST turnover includes proceeds from the sale of capital assets, unless the sale is input taxed. Current GST turnover includes taxable and GST-free supplies, but should exclude input taxed supplies such as residential rental income and financial supplies like dividends, interest etc. JobKeeper and ATO cash flow boost payments should be excluded from the calculation along with other payments that don’t represent consideration for a supply made by the entity such as certain State based grants.

The Commissioner of Taxation has the power to set out alternative tests that establish eligibility in specific circumstances where it is not appropriate to compare actual turnover in a quarter in 2020 with actual turnover in a quarter in 2019. The Commissioner provided a number of alternative tests that could be used for passing the original decline in turnover test and the ATO has indicated that similar tests are likely to be available for the additional decline in turnover tests for the September 2020 and December 2020 quarters, but these have not been released as yet.

A number of modifications apply to not for profit entities when it comes to calculating GST turnover under the original decline in turnover test. It appears that the same modifications will generally also apply when determining whether a not for profit entity passes the new decline in turnover tests for the September 2020 and December 2020 quarters.

To be eligible to receive JobKeeper payments, the employer must meet a wage condition. That is, employers must have paid the eligible employee at least the applicable JobKeeper payment for the relevant fortnight.

The ATO reimburses the employer for the JobKeeper payment monthly in arrears.

As noted above, for the JobKeeper fortnights starting 28 September 2020 and 12 October 2020 the ATO is allowing employers until 31 October 2020 to meet the wage condition for all employees included in the JobKeeper scheme.

From 3 August 2020, the eligibility tests for employees were changed to enable a greater number of employees to access JobKeeper.

Previously, an employee had to be employed by the relevant entity on 1 March 2020 to be eligible for JobKeeper payments. Someone employed as a casual on that date also must have been employed on a regular and systematic basis for the 12 month period leading up to 1 March 2020.

Now, employees who were previously ineligible for JobKeeper because they were not employed by the entity on 1 March 2020 may be able to receive JobKeeper payments if they were employed by the entity on 1 July 2020 and can fulfil all of the other eligibility requirements. If an employee already passed all the relevant conditions at 1 March 2020 then they don’t need to be retested using the 1 July 2020 test date.

On 1 July 2020 (previously 1 March 2020):

Was aged 16 years and over; and

If the individual was aged 16 or 17, was either financially independent or was not undertaking full-time study;

Was an employee other than a casual, or was a long-term casual*; and

Was an Australian resident (under the meaning of the Social Security Act 1991), or a resident for tax purposes and held a Subclass 444 (Special category) visa**.

And, at any point during the JobKeeper fortnight:

Was an employee of the employer (including employees that have been stood down or rehired); and

Was not an excluded employee:

An employee receiving parental leave pay or dad and partner pay; or

An employee receiving workers compensation payments in relation to total incapacity.

Agreeing to be nominated by the employer as an eligible employee under the JobKeeper scheme; and

Confirming that they have not agreed to be nominated by another employer; and

If they are a long-term casual, they do not have permanent employment with another employer.

*A ‘long term casual employee’ is a person who has been employed by the business on a regular and systematic basis during the period of 12 months that ended on the applicable testing date (previously 1 March 2020, but changing to 1 July 2020). These are likely to be employees with a recurring work schedule or a reasonable expectation of ongoing work.

The 28 days finishing on the last day of the last pay period that ended before either: 1 March 2020, or1 July 2020.

Actual hours worked including any hours for which they received paid leave (e.g., annual, long service, sick, carers and other forms of paid leave) or paid absence for public holidays. An employee’s ‘actual’ hours might be different to their contracted, ordinary hours or hours they are paid for.

Eligible business participants

February 2020 (29 days)

Active engagement in the business.

Religious practitioners

February 2020 (29 days)

Activities in pursuit of your vocation for your institution.

Eligible employees that have been employed on a full time basis since 1 March 2020 or 1 July 2020 will generally receive the higher JobKeeper rate (as full time employees work more than 80 hours in 28 days) .

Businesses however will need to determine the rate applicable to eligible part-time and casual employees.

The reference period is the 28 day ending at the end of the most recent pay cycle for the employee ending before:

1 March 2020; or

1 July 2020.

For eligible employees who have been employed since 1 March 2020, employers need to choose the reference period that provides the best outcome for the employees. For many employers, this will be the pre COVID-19, 1 March 2020 reference date.

For eligible employees employed since 1 July 2020, use the pay periods prior to 1 July 2020.

If the pay cycle is longer than 28 days, a pro-rata calculation needs to be done to determine the average hours worked and on paid leave across an equivalent 28 day period. For example, if the relevant monthly pay cycle has 31 days, you take the total hours for the month and multiply this by 28/31.

In order for an employer to receive JobKeeper payments from 28 September 2020 onwards they must notify the ATO of the payment rates for all eligible employees. The employer must then notify its employees within 7 days of advising the ATO of the payment rate.

Example – fortnightly pay cycle Emma has been a permanent part-time employee of a bus company since 2010. The company has a fortnightly pay cycle ending on Fridays. The bus company is an eligible employer as they have suffered a decline in turnover of more than 30%. Using the company’s payroll cycle, Emma’s hours for the 1 July 2020 reference period are: Payroll periodWeekHours 23 May 2020 to 5 June 2020 Week 1 20 Week 2 19.5 6 June 2020 to 19 June 2020 Week 3 20 Week 4 19 annual leaveTotal hours78.5 Emma’s annual leave in February is included in her total hours as any hours for which an employee received paid leave (e.g., annual, long service, sick, carers and other forms of paid leave) or paid absence for public holidays, are included. Continued over…

Emma’s hours for the 1 March 2020 reference period are: Payroll periodWeekHours 1 February 2020 to 14 February 2020 Week 1 20 Week 2 22 15 February 2020 to 28 February 2020 Week 3 20 Week 4 19 Total hours81 Assuming the bus company continues to be eligible for JobKeeper payments, the company is eligible to receive the higher rate of $1,200 per fortnight between 28 September 2020 to 3 January 2021 for Emma, and $1,000 per fortnight for 4 January 2021 to 28 March 2021 assuming Emma remains employed. This is because Emma worked 80 hours or more for the 1 March 2020 reference period. Had she worked less than 80 hours, she would be eligible for the lower rate of JobKeeper. Adapted from the Explanatory Statement

Example – monthly pay cycle Antonio has been a permanent employee of a Lai Industries since 2010. The company has a monthly pay cycle that ends of the 15th of each month. The company is an eligible employer as they have suffered a decline in turnover of more than 30%. Using the company’s payroll cycle, Antonio’s hours for the 1 July 2020 reference period are: Payroll periodHours 16 May 2020 to 15 June 2020 (31 days) 85 Total hours over payroll period85Total hours over 28 day reference period76.8 As the reference period is 28 days, Lai Industries need to pro-rata Antonio’s hours. 28 days/ 31 day payroll period x 85 (total hours worked over payroll period) = 76.8 hours. Continued over…

Antonio’s hours for the 1 March 2020 reference period are: Payroll periodHours 16 January 2020 to 15 February 2020 (31 days) 85 worked 80 leave Total hours over payroll period165Total hours over 28 day reference period149 28 days/ 31 day payroll period x 165 (total hours worked over payroll period) = 149 hours. Assuming the Lai Industries continues to be eligible for JobKeeper payments, the company is eligible to receive the higher rate of $1,200 per fortnight between 28 September 2020 to 3 January 2021 for Antonio, and $1,000 per fortnight for 4 January 2021 to 28 March 2021 assuming Antonio remains employed. Adapted from the Explanatory Statement

There reference period is not typical of the employee’s hours or you use a rostering system and there is no typical pattern in a 28 day period; or

The employee started work during the reference period.

Reference period not typical

Where the reference period is not typical of an employee’s hours, for example they took unpaid leave, or your business was in a drought or bushfire zone, or the employee was stood down etc., you can use an earlier 28 day period or multiple 28 day periods that more accurately represent the employee’s typical arrangements.

The reference period becomes the 28 day period ending at the end of the most recent pay cycle for the employee before 1 March 2020 or 1 July 2020 in which the employee’s total number of hours of work, of paid leave and of paid absence on public holidays was representative of a typical 28-day period. That is, you select the next 28 day period before 1 March 2020 or 1 July 2020 that represents the employee’s typical employment pattern.

Example – alternative payroll period George has been a permanent part-time employee of a restaurant since 2018. The company has a fortnightly pay cycle ending on Fridays. The restaurant is an eligible employer as they have suffered a decline in turnover of more than 30%. George did not work in May or June 2020. Using the company’s payroll cycle, George’s hours for the 1 March 2020 reference period are: Payroll periodWeekHours 1 February 2020 to 14 February 2020 Week 1 18 Week 2 22 15 February 2020 to 28 February 2020 Week 3 0 unpaid leave Week 4 24 Total hours64 George typically works a minimum of 18 hours in any given week. However, in week 3, George took unpaid leave. As week 3 is not typical of George’s arrangement, the restaurant uses another 28 day period before 1 March 2020 that is typical of his arrangements. Payroll periodWeekHours 4 January 2020 to 17 January 2020 Week 1 24 Week 2 18 18 January 2020 to 31 January 2020 Week 3 22 Week 4 24 Total hours88 Using the alternative test, George is eligible for the higher JobKeeper rate.

For workers that don’t have a typical pattern because of a rostering system like fly-in-fly-out workers, an average of the hours worked over the employee’s rostering schedule and proportionally adjusted over 28 days can be used to work out a typical 28-day period.

Employee started work during the reference period

Where an employee started work during the 28 days prior to either 1 March 2020 or 1 July 2020, you can use a forward-looking alternative test. In these circumstances, use the pay cycle immediately on or after 1 March 2020 or 1 July 2020. For employers with fortnightly or weekly pay cycles, you must use consecutive weeks.

Where an employee was stood down, use the first 28 day period starting on the first day of a pay cycle on or after 1 March 2020 or on or after 1 July 2020 in which they were not stood down.

Sale of business or changes within a group

Where the business changed hands or the employee changed employment within a wholly owned group, the hours worked with the previous employer cannot be counted. Instead, use the pay cycle immediately on or after 1 March 2020 or 1 July 2020. For employers with fortnightly or weekly pay cycles, you must use consecutive weeks.

If the employee has been stood down, use the first 28 day period starting on the first day of a pay cycle on or after 1 March 2020 or on or after 1 July 2020 in which they were not stood down.

Some employees will automatically qualify for the higher JobKeeper payment rate. Broadly, this applies if the employer has incomplete records of total hours of work and paid leave, including where salary, wages, commissions, bonuses etc are not tied to an hourly rate or contracted rate.

The employee must also fall within specific categories, including:

They were paid at least $1,500 in the reference period;

They were required to work at least 80 hours under an industrial award, enterprise agreement or contract; or

It is reasonable to assume that they worked at least 80 hours during the applicable period.

The reference period for business participants is the month of February 2020 (the whole 29 days).

A business participant is a sole trader or self-employed with an ABN, or one partner in a partnership, adult beneficiary of a trust, director or shareholder who works in the business (i.e., only one person in a partnership, one beneficiary of a trust, or one director / shareholder can be eligible for JobKeeper payments for a particular entity).

The test to determine eligibility is based on the hours of active engagement in the business carried on by the entity. This requires an assessment of the hours that the business participant was actively operating the business or undertaking specific tasks in business development and planning, regulatory compliance or similar activities in an applicable reference period.

Other than sole traders and self-employed, a business participant must provide a declaration to the business entity confirming their hours worked over the reference period.

For JobKeeper payments from 28 September 2020, the business must notify the Tax Commissioner about whether the higher or lower rate applies to the business participant and notify the participant within 7 days of providing this notice to the Commissioner.

Where February 2020 was not typical of the participant’s hours, an alternative test can be used:

Not typical – use the next typical 29 day period

Commenced work during February 2020 – use March 2020

Not employed by the employer but still an eligible religious practitioner for JobKeeper purposes – use March 2020

The reference period for eligible religious practitioners is the month of February 2020.

A religious practitioner is a minister of religion or a full time member of a religious order who undertakes activities in pursuit of their vocation as a member of a religious institution.

The payment rates are based on the number of hours they spent doing an activity, or series of activities, in pursuit of their vocation as a religious practitioner as a member of the religious institution in the reference period. For example:

Performance of the rituals or practices of the religious institution (including participation in services, prayer, contemplation or meditation, insofar as they constitute such rituals or practices); and

Furtherance of the objectives of the religious organisation (including missionary or charitable work, insofar as they constitute such an objective).

The religious practitioner must provide a declaration to their institution confirming their hours worked over the reference period.

For JobKeeper payments from 28 September 2020, religious institutions must notify the Tax Commissioner about whether the higher or lower rate applies to each of their eligible religious practitioners and notify the practitioner within 7 days of providing this notice to the Commissioner.

Where February 2020 was not typical of the practitioner’s hours, an alternative test can be used:

Not typical – use the next typical 29 day period

Commenced work during February 2020 – use March 2020

Not employed by the employer but still an eligible religious practitioner for JobKeeper purposes – use March 2020

The super guarantee (SG) means that if you are in full-time employment your employer pays a minimum amount (currently 9.5%) into your super account. You can view your super and investment portfolio via an online platform provided by your superannuation fund. While knowing your super balance is important, understanding your superannuation risk profile – and acting on this knowledge – could make a difference to the amount you have when you want to retire.

Lara Bourguignon, General Manager of Customer Experience at MLC, warned against the “set and forget” mentality of some people to super:

“Being in the right super risk profile is one of the key factors that will determine how much you have when you retire, but it’s often overlooked.”

Until last year, if you did not select what type of investment strategy you preferred (ie, high-risk/ high-return, or lower risk/stable return) your money would automatically go into a default fund. From July 2017, however, super funds were obligated to transfer monies from default funds into a MySuper account. Thus, no distinction is made whether you are an aggressive investor, or, at the other end of the scale, a passive one, as you are placed automatically in a low-cost fund with a diversified investment strategy; it is, therefore, a good idea to select your own super risk profile.

Understanding your super risk profile

The amount of financial risk you can take is linked to your life circumstances. Accordingly, you can decide to take conservative, moderate, or aggressive risk in terms of investment and each will lead to different returns. Generally, the younger you are, the greater financial risk you can take in terms of investing because you have longer to make up any shortfall. Looking at your super risk profile will show where you sit on the investment risk-taking spectrum.

“If there’s one thing every Australian can do right now to improve their retirement it’s to get in touch with their super fund and check what risk profile they are in, and, if it’s not right for them, adjust it,”

The latest survey has highlighted a general lack of awareness among respondents that could be contributing to a shortfall in super. Young women are particularly at risk, with 45 percent being unaware of their super risk profile.

The following example was given by MLC:

A woman aged 25 on $80,000 a year who has a conservative risk profile until she is 70 could improve her super balance by around as much as $294,000 if she knew and adjusted her profile according to her circumstances and life stage.

How to fix your super risk profile

We may be able to help you with advice on how to adjust your risk category to get the most you can out of super. Please contact us to discuss your circumstances and find out how we can assist further.

Historically, cash has been the preference for many Australian businesses. Unfortunately, this also made it very attractive for businesses to “forget” to disclose some of their cash-in-hand earnings. When cash is not banked, it’s very hard to trace. This meant that a lot of the participants of the cash economy were able to get away with tax avoidance and even getting around employment laws.

undeclared income costs the Australian economy an estimated $15 billion in lost taxes and welfare payments each year.

There are many businesses in the cash economy that do the right thing, but unfortunately because of the “bad apples,” all businesses in the cash economy have come under the microscope of the Tax Office and other government departments.

Now how does this affect you? What are some of the industries being focused on? And what are some of the ways you can safeguard yourself against this crack down on the cash economy?

Who is the ATO targeting?

Some of the industries the ATO is focusing on are cafes and restaurants, carpentry and electrical services, hair, beauty and nail specialists, building tradespeople, road freight businesses, waste skip operators and house cleaners.

Typically there are three types of problem businesses and individuals in the cash economy:

businesses and people who don’t understand the law;

businesses and individuals who deliberately avoid their tax obligations; and

people who use cash payments to hide income, to avoid losing Centrelink payments, or who are breaching visa restrictions.

A key tool the ATO will be using to catch avoidance in the cash economy is data-matching programs. The ATO has created profiles of businesses based on their various characteristics. This allows them to benchmark and compares its income, profit margins and level of profitability with similar others. If a business falls outside these benchmarks they are more likely to get audited. Audits can be expensive and time-consuming even if you haven’t done anything wrong and have a legitimate reason for falling outside the ATO benchmarks. It is important to ensure your accountant has checked that you are within the benchmarks for your industry, sometimes choosing the correct industry code may be the difference between being audited or keeping clear of the ATO’s radar. For example, Let’s say a business earns income predominantly from selling goods (but also earns income from rendering services). When the tax return is done for this business, the business code that is chosen for the service industry (in which the business does not earn the majority of its income). The ATO will end up comparing this business against other businesses in a completely different industry which is likely to lead the ATO to the deem it to have fallen outside the industry benchmarks.

Incentives to move away from cash are on the horizon. As part of its terms of reference, the Federal Government’s Black Economy Taskforce will look into possible tax and other incentives for small businesses that adopt a non-cash business model.

How can you safeguard your business?

The first place to look in terms of safeguarding your business is your bookkeeping. Make sure sales and purchases are recorded accurately (ideally in an accounting software). Make sure you issue invoices when a sale is made and that you keep purchase invoices on file. This will give you a clear audit trail to prove that you are declaring all income. Most importantly make sure you have an open line of communication with your accountant and ask them questions about how you can keep your business out of the ATO firing line.

Every thought if you are getting the best returns from your investment property? This guide will help you evaluate the returns. Let’s find it out.

Property depreciation claims

Depreciation works to lower your taxable income, meaning that you pay less tax, which can help boost your return. To make it less cumbersome, the ATO allows you to claim depreciation using low-value asset pooling. This means you do not have to account for the depreciation for each asset separately, but rather pool all the assets together and claim depreciation on the pooled asset value.

What are depreciable assets?

Depreciable assets for an investment property include both items within the building, classed as “plant and equipment”, and the “building” itself. Plant and equipment covers items such as ovens, air-conditioners and carpets, and building includes construction costs for items such as brickwork and concrete. Common property, for example stairways and gardens, can also be included as part of the building.

How to determine asset values

Before we can help you assess your claim, you will need to have your property valued by a qualified quantity surveyor. As construction and property depreciation is a specialised field, accountants are unable to make estimates on construction costs.

As part of the valuation, the surveyor will need to conduct a site inspection and photograph and log all items in a report. The optimum time to do this inspection is after settlement, and before your tenant moves in. Note, too, that it may take a couple of weeks for the surveyor to prepare the report.

The surveyor’s report will allow us to work out the depreciation type and schedule. The good news is that surveyor fees are tax deductible too!

Even with talk of bubbles bursting and budget-time reforms, property remains a popular choice for investors. An investment property can bring more savings at tax time through property depreciation deductions than many people – particularly new investors – realise.

Factors to consider for the depreciation schedule

Age of building

How old is the building? This will determine which costs can be included in your depreciation schedule. If it was built post-1985, then plant and equipment and building costs can be depreciated. If it was built before 1985, then you can only claim for plant and equipment.

Property purchase date

Did you buy the property a few years ago? This doesn’t mean you have to miss out on the depreciation savings – if deductions are available, we can go back and amend your previous tax returns.

Renovations and repairs

Renovation expenses can be included, but we’ll need to know the amount of these costs. You’re also entitled to claim depreciation even if the renovations were completed by the previous owner. But as with the primary valuation, if you don’t know the cost of the renovations, then a quantity surveyor will need to make that estimation.

Keep in mind that repairs and improvements made to the property before it is leased can’t be claimed in the depreciation schedule, because the costs are incurred before the property is generating income.

Also, some items which you might think are fixtures, such as cupboards, are actually classified as part of the building, and so the expense of replacing them can’t be claimed as a depreciable asset under Div 40 of the Income Tax Assessment Act 1997. However, a percentage of the cost of installation by a tradesperson can be claimed as capital expenditure. The claimable amount will be influenced by the tradeperson’s profit margin.

Contact us

Talk to us to find out more about your obligations, entitlements and other considerations when working in the gig economy.

This is the first article in our series on the gig economy, where we explore the changes in the employment market, and the related tax and financial issues that workers and employers face.

What is the gig economy?

The gig economy is characterised by freelance and project-based work. Its players inhabit a constantly changing workscape and juggle a pastiche of jobs.

In some circumstances, gig economy workers have very little connection with their “employers”. This is typical for the “share economy” workers of Uber, Airtasker and similar companies, where the platform owner facilitates jobs through a technological medium like a website or an app, and the workers pay a percentage of their earnings for access.

But many gig workers make their living through a combination of employee and freelancer jobs. Sometimes known as “slashies” (for the slashes in their multifaceted career descriptions), these people often work across multiple industries and offer a diversity of skills and experience. A slashie might be, for example, a university tutor/web designer/bartender.

If you are a solopreneur, a casual employee, a contractor or a slashie, the chances are that you are part of the gig economy.

Got a gig?

While recent changes in the labour market have brought flexibility for both employers and workers, they have also brought risk and uncertainty. For many, too, there is an increase in the amount of administration they must do for contracts, recordkeeping and their income stream, as well as greater complexity in planning a financial future.

Each employment type, task and industry has unique characteristics and implications for tax and financial planning. But regardless of the category, similar tax, superannuation and income contingency planning considerations apply. We can help you manage these.

The impact of the gig economy on the employment market and the economy as a whole is yet to be realised, as are the social effects, yet it is touted as the future of work. Many more of us are likely to find ourselves as players. So why not have an advantage? Understanding your obligations and entitlements and having a plan for stability in this dynamic market is critical for success.

Employment status

Are you an employee, a contractor, self-employed – or is your work a combination?

If you are part of the gig economy, then it is essential to establish your status for each job. Fair Work Australia provides a clear summary based on the level of control you have in carrying out the work and responsibility for statutory obligations such as taxes and benefits.

As an employee, you will have pay-as-you-go (PAYG) tax deducted from your wages, and superannuation and other benefits will be paid by your employer. Your contract will specify if you are a casual, fixed-term, or permanent employee. Employees also have the benefit of workers compensation if they are injured on the job.

For any work you undertake as a contractor, you have responsibility for managing your own obligations, including your tax, superannuation and insurance.

Tax

Determining your tax status will be more complex if you have multiple gigs.

If you are a PAYG employee but also use an Australian Business Number (ABN) to invoice for other work, you will need to lodge an annual personal tax return and may also have to lodge a regular Business Activity Statement (BAS) and pay tax instalments. You will need to set aside funds out of the income from your invoiced work to make your BAS payments. These tax instalments are usually required quarterly, and it’s a good idea to set aside around 35% of each income payment you receive.

To further complicate things, if you derive income from your individual skills or personal efforts – for example, if you are an entertainer, engineer or IT consultant – you’ll need to work out if you are classified as a personal services business (PSB) and/or you earn personal services income (PSI). This is significant, as there are substantial differences between the corporate and personal tax rates and the deductions claimable for the different income types. Accurately identifying your PSI/PSB status can be tricky, depending on your profession, how you are contracted and the scope of your work, especially where you have multiple contracts.

GST registration

If you earn more than the $75,000 threshold through your ABN, you need to register for Australian GST. And if you earn income as an Uber driver, you are now required to register for GST no matter how much (or little) you earn from that work. If this applies to you, talk to us about whether you can use your existing GST registration.

For everyone else who works in the platform economy – watch this space! The Federal Government is setting its sights on better ways of capturing GST on consumption, as we’ve seen with the introduction of the “Netflix tax” on digital products and services and the proposed low-value imported goods tax.

Superannuation

You’ll also need to manage your own superannuation for your gig-economy income, whether you divert money into an existing fund or set up a self managed super fund (SMSF). An SMSF may be worth considering if you’re looking for greater portability and diversity in investments.

Insurance

PAYG employees are covered for workers compensation by their employer. If you are a contractor or run a small business you will have to take out you own insurance to cover loss of income, illness, disability and death, and possibly other insurance types if you also employ people (workers compensation), sell products or provide certain services (professional indemnity).

Deductions

Negotiating entitlements for cross-industry work and a variety of tasks can be bamboozling. We can help make sure that you’re claiming appropriately for your types of work and business.

Some common issues faced by gig economy workers include distiguishing between revenue and capital expenses, and apportioning claims where assets are for both personal and professional use. Don’t forget that if you’re undertaking project work, you might be entitled to claim for coworking space hire, software that allows for collaboration across a team, travel expenses and equipment depreciation.

As always, good recordkeeping is essential – hold onto all of your receipts!

Charging clients and low season contingency plans

If you’re a sole trader or casual employee, the level of control you have over the rates you charge will vary according to your profession and from gig to gig. Nonetheless, it is essential to build into your fee structure the amounts you need to cover your tax, superannuation, insurance, purchasing new equipment, training, any certification fees, repairs.

Balancing current work while chasing future work and keeping up with tax and other obligations can be extremely challenging. You should also plan how you’ll deal with periods when you’ll have less work and income, and think about how to fund some holiday time. Talk to us if you’d like help developing a contingency plan.

Every business runs using a particular legal structure – as a sole trader, a partnership, through a company or trust arrangement or even using a combination of these structures. Each structure offers different advantages and disadvantages. These advantages range from ease of regulatory compliance to matters of personal liability to asset protection considerations and, of course, tax advantages and requirements. The “mere” choice to operate a business using a particular structure for its beneficial tax outcomes does not generally amount to tax avoidance.

In this increasingly complex and fast-changing commercial and trading world, you may find it necessary to change your business’s form from one structure to another as business (or personal) needs shift. There are a range of tax concessions that allow for a change in business structure without triggering tax liabilities that may otherwise arise on the transfer of business assets from one structure to another – particularly in relation to capital gains tax (CGT).

For example, from its inception, the CGT regime has provided for “CGT rollover” relief when a business’s assets are transferred from a sole trader or partnership structure to a wholly owned company structure (with all the tax and other benefits that could arise from running a business as a company).

Likewise, rollover relief is available when interposing a company or a trust between a business’s owners and the existing entity through which the business is run, if this considered to be a viable thing to do for the business.

A CGT rollover allows you to "roll over" a capital gain connected to a CGT event,

such as the transfer of assets from a sole trader business to a company business

in a restructure.This means you can put off paying tax on the gain until another

CGT event happens to the assets – for example, when the company sells them.

The small business restructure rollover (which applies to transfer of assets occurring from 1 July 2016) was introduced to provide greater flexibility for businesses with a small aggregated turnover of (at the time of writing this article this amount was $2 Million). This rollover is somewhat revolutionary, because for the first time it allows business assets to be transferred to a discretionary trust, subject to the underlying principle of any business CGT rollover, which is that the ultimate ownership of the assets does not change. In effect, the rollover rules themselves are designed to maintain the economic ownership of the transferred business assets in various ways, including through the use of “safe harbour” rules.

This small business restructure rollover provides tremendous scope for business owners to restructure their business in a variety of ways without triggering CGT (or other) tax liabilities.

However, as with the other business rollovers available, a restructure must meet a range of conditions for the new rollover to apply. The key conditions are as follows:

the transfer of the assets must be part of a “genuine restructure” of an ongoing business;

the entities involved in the restructure must, in effect, be “small business entities” in terms of the $2 million annual turnover test (this threshold is proposed to change to $10 million);

the transfer of the assets must not materially change the “ultimate economic ownership” of the assets transferred;

the asset transferred must be an active asset (ie one used or held ready for use in carrying on a business);

the transferor and transferee parties must be Australian residents for tax purposes (at the time of the transfer); and

the transferor and each transferee must choose to apply the rollover.

Each of these requirements have their own particular intricacies that must be considered carefully in light of the particular business’s and taxpayer’s circumstances. For example, the requirement that the restructure be “genuine” means that it cannot be undertaken as or be part of an “inappropriately tax-driven scheme” – for instance, one that allows the transferred assets to later be sold with minimal tax consequences. This requirement is so significant that the ATO has issued a lengthy guide, Law Companion Guide LCG 2016/3, to illustrate what would and would not be regarded as a “genuine restructure”.

In spite of the need to meet these varied and precise conditions, this rollover will prove invaluable for business taxpayers who find it necessary to change the legal structure of their business to fit in with their changing business and the shifting domestic and global business environment.

Contact us

Are you considering changing the structure of your business, or wondering about other CGT-related matters? Contact us to talk about your situation.

In a commercial context, where a creditor has made a loan that the debtor uses in the course of a business or to produce their assessable income, there will be clear capital gains tax (CGT) consequences when the creditor agrees to forgive the debt. This is because the creditor’s legal or equitable right to repayment of a debt is a CGT asset in the creditor’s hands.

However, this does not necessarily mean that the creditor will make an outright capital loss on the forgiveness of a debt equal to the amount of the debt owed. There will be other factors to consider, including whether the debt is entirely forgiven and the circumstances under which it is forgiven. The debtor’s capacity to repay the debt (that is, the extent to which the debt is “truly bad”) will have a significant bearing on the amount of any capital loss arising to the creditor – and could even mean that the creditor makes no capital loss. The “truly bad” status of a debt can be complicated to determine, depending on the particular circumstances of the creditor, the debtor, the debt and the forgiveness arrangement.

Whether the parties are dealing with each other at “arm’s length” under the forgiveness arrangement (and not just in terms of whether they are related parties) will likewise have a significant bearing on the amount of any capital loss arising to the creditor. This consideration is typically important where the parties are a shareholder and a wholly owned company.

Where a debt exists as part of a private (non-commercial) arrangement – such as a loan between family members – and is forgiven, there are a range of other CGT-related matters to consider. In particular, the tax consequences will depend on whether the loan was made at a commercial rate of interest or is interest free. As a basic rule, however, where a loan was not used to produce assessable income, the lender’s forgiveness of the debt does not give rise to a capital loss.

The debtor’s capacity to repay the debt will have a significant bearing on the amount of any capital loss arising to the creditor – and could even mean that the creditor makes no capital loss.

The debtor’s position: having a debt forgiven

In a commercial arrangement where a debt is forgiven – that is, one where interest was payable on the loan – the forgiven debtor’s position involves a range of entirely different CGT considerations.

This is because, unlike the creditor, the debtor does not own a CGT asset as part of the debt arrangement. The debtor’s repayment obligations are merely that: obligations or liabilities, but not assets.

Nevertheless, a debtor obtains a type of commercial or other advantage when their repayment obligations are forgiven, waived, released or extinguished. To take this into account, the tax law includes special rules that aim to indirectly recoup the debtor’s tax advantages associated with forgiveness of the debt, to the extent that the debt was a commercial arrangement.

Generally, these rules provide for the net amount forgiven to be deducted from certain current and future tax deductions the debtor claims. Specifically, the net forgiven amount of the debt reduces the following tax deduction amounts, in this order:

the debtor’s prior year revenue losses;

the debtor’s prior year net capital losses;

undeducted balances of other expenditure that the debtor carries forward for deduction (including depreciable assets); and

the CGT cost base of other assets that the debtor holds.

In short, a taxpayer does not get off tax-implication free when a creditor forgives a debt they owed under a commercial arrangement.

Contact us

The CGT and other tax consequences related to debt forgiveness can be difficult to navigate, for both the creditor and the debtor, and will depend on the specific circumstances surrounding the matter. Contact us if you would like more information about how forgiving a debt, or having a debt forgiven, may affect your tax situation.

The main areas for travel expenses that can be claimed as tax deductions are:

transport;

meals; and

accommodation.

Specifically, these can include:

public transport costs, including taxi and air travel fares;

bridge and road tolls, parking fees and short-term car hire costs;

meals and accommodation expenses while staying overnight for work;

incidental expenses for purchases that are linked to your work and the purpose of the work trip; and

petrol, oil and repair costs for a car that is owned or leased by someone else.

However, there are a number of factors to keep in mind when claiming travel-related deductions in your personal income tax return as an individual or as part of small business.

What is “work-related”?

Defining what is work-related is an essential consideration for all travel claims. There must be a direct link between your work and the expense. Put simply, you need to ask: is the travel linked to producing the income on which you pay tax?

Transgressions by politicians aside, recent cases have highlighted the importance of correctly establishing the relationship between your work and the claimed expenses. It’s also important to ensure that your employer will support your claim, should the ATO ask them. In the case of Re Vakiloroaya and FCT [2017] AATA 95, the ATO denied the taxpayer’s claim for $60,000 of work expenses, including travel, and the Administrative Appeals Tribunal agreed, in part because the taxpayer’s travel to visit clients was not required by his employer as a core part of his work.

Thresholds for deductions

To help taxpayers successfully claim reasonable deductions, each year the ATO publishes a Taxation Determination that sets out the amounts considered reasonable to claim for various travel destinations in that income year (for example, see TD 2016/13 for the 2016–2017 income year). This provides a useful baseline for trip budgeting and claiming deductions.

Expenditure versus allowances

Another important question to ask is whether you are paying for work-related travel out of your own pocket – or has your employer paid you a travel allowance?

If you are footing the bill for work-related travel yourself, then the expenses can be claimed as deductions on your tax return. However, if your employer reimburses you for the costs, you cannot also claim them.

A slightly more complex situation comes about if your employer has paid you an allowance. You will most likely have to declare the allowance as income in your tax return, especially if the amount is over the threshold set out as reasonable in the relavent year’s tax determination. Your employer is required to withhold tax on this payment as on your salary. If you are a small business owner who pays an allowance to your employees, your accountant can provide further advice on the finer points of your tax and declaration obligations.

Substantiating your claims

If you are claiming travel expenses, you need to maintain evidence to back your claim. Keeping receipts and information such as a log of car expenses, dates, driving distances and fuel purchases is vital. To show that claimed expenses are work-related, keep a travel diary recording the details of business meetings, including dates, durations, places, times and activities. In addition, sending follow-up email to clients detailing pertinent actions arising out of your meetings offers useful support for your claims.

Distinguishing between business and pleasure

Extending a business trip to include a holiday is a very popular approach, for good reason – it’s an excellent way to get the most out of a trip. However, you need to ensure that you only claim deductions for the work components of your trip. Again, keeping a travel diary will help in keeping your claims organised and reasonable.

Claiming expenses of travelling companions

The interesting case of Re WTPG and FCT [2016] AATA 971 highlighted issues with claiming travel companions’ expenses. If you are considering doing this, it’s worth discussing with your tax adviser when planning your travel. In this particular case, a taxpayer with disabilities was denied a deduction for his wife’s travel costs when she accompanied him to conferences overseas. The taxpayer’s wife had accompanied him on the trip as a carer, as his employer did not provide one. The ATO ruled that his wife’s travel expenses were not related to income-producing activities and so could not be claimed as deductions, and the Administrative Appeals Tribunal agreed with that ruling.

The super guarantee (SG) means that if you are in full-time employment your employer pays a minimum amount (currently 9.5%) into your super account. You can view your super and investment portfolio via an online platform provided by your superannuation fund. While knowing your super balance is important, understanding your superannuation risk profile – and acting on this knowledge – could make a difference to the amount you have when you want to retire.

The super guarantee (SG) means that if you are in full-time employment your employer pays a minimum amount (currently 9.5%) into your super account. You can view your super and investment portfolio via an online platform provided by your superannuation fund. While knowing your super balance is important, understanding your superannuation risk profile – and acting on this knowledge – could make a difference to the amount you have when you want to retire.